The Challenge

- Lenders are continuing to struggle with the rising cost associated with the adoption of new mortgage life cycle frameworks, new regulation looming such as a revised HMDA rule, flood rule changes, the aftermath of TRID implementations, proposed CFPB servicing rules and top of that the board’s focus on risk and compliance processes are forcing mortgage lenders to go through major modification of their internal control programs. This one client, mentioned in the case study below was going through similar challenges.

- When a mortgage organization is doing massive amounts of audits and risk assessments, it struggles with the quality of data to assess especially if the organization has manual or duplicate lending processes around risk assessments for measuring the efficacy of its internal controls.

- Many mortgage organizations are learning the hard way that their manual or automated enterprise risk or operational risk management systems are less productive in meeting their challenges for internal control management.

The Solution

- There are certain things that humans just can’t do or catch no matter how many people you throw at the problem. The solution involved in using artificial intelligence to automate measurement of “efficacy metrics” based on internal control effectiveness.

- Automate the system to take a data feed from systems mortgage systems or customer supports systems, calculate the value and assess if the controls are effective or not and make changes to the efficacy of the internal controls through automation.

- Instead of doing audit once a year, you have greater visibility of the effectiveness of internal controls over the course of the year. This way when an examiner walks in , he/she does not have to do your work in finding out whether the control is effective or not.

Value

- The value in automating the efficacy of your internal controls lies in substantial cost reduction. Instead of investing in hundreds of people to measure the effectiveness of their internal controls, the system can do that job and the company can reallocate those resources into other functional departments considering skilled mortgage risk and compliance resources are hard to find.

- Further there are certain things that humans just can’t catch or do. The quality of efficacy of internal control data would substantially increase.

A Case Study

Challenge

- One mortgage lending industry client that we were working with was going through similar challenges mentioned above.

- They were doing massive amounts of audits, risk assessments and struggled with the quality of data to assess if their internal controls are effective or not since most of the process around risk assessments and measuring the efficacy of their controls was manual

- They had to continue to throw more people at their problem ( in the hundreds) towards efficacy metrics i.e to measure controls effectiveness which substantially increased the cost in addition the quality of the efficacy of internal controls was also in question.

Solution

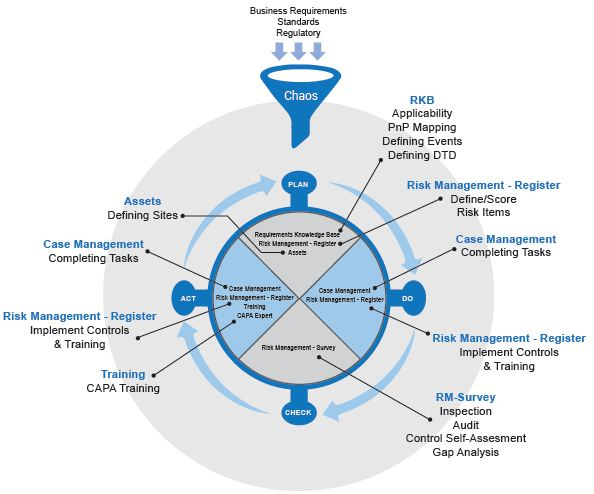

- The Predict360 enterprise risk and compliance management system was configured to read internal control data either directly through a feed or through a common input interface where no feed is available. This asset level disclosure data was then mapped and processed via a rules engine to determine and then update control efficacy.

- For example, if a control has its efficacy target set on a scale: values 400 – 600 equivalent to efficacy of 0-100% effective, and the input value is 500, then the efficacy for the associated control would be 50%

If you would like a complimentary 60-minute advice on Automating Regulatory Change Management or would like for us to do a proof of concept for, please contact us