Home/ Blog / Explore the Intricate Synergy of Internal Audit and Risk Management

It has been critically observed that a couple of functions stand out for their essential role in safeguarding organizational sustainability and integrity: internal audit and risk management. While each offers a unique realm of opportunities, their combined benefit is undeniable. Aggregately, they create a holistic shield, protecting a company from possible environmental hurdles while guaranteeing compliance and operational excellence.

Financial enterprises experience various risks, compliance obligations, and regulatory requirements that can noticeably influence their operations and reputation. Companies depend on several control functions to reduce these risks and ensure adherence to compliance, including internal audit and risk management. These functions have distinct roles and responsibilities, but both aim to enhance organizational performance. By working collaboratively, internal audit and risk management functions can make a synergy that enhances corporate value in different ways.

Despite such benefits, these departments often work in silos in many corporations, with little collaboration and communication.

Overview of Risk Management and Internal Audit

Risk management is a critical component of an organization’s governance, risk, and compliance program. It involves the risk department’s actions to recognize, assess, manage, and control potential threats. These range from specific project-related risks to an organization’s broader economic challenges. An effective risk management program helps a company define its risk appetite and improves strategic decision-making. Leaders can ensure constant internal communication regarding risks by employing the appropriate risk management frameworks.

Within an effective internal audit and risk management framework, internal audits are essential for ensuring that an organization’s controls and monitoring functions are efficient, compliant, and up-to-date with internal processes and external regulations. One of the foundational accountabilities of internal auditors is to evaluate the efficacy of enterprise internal procedures and controls.

Auditors conduct continuous evaluations periodically to ensure that the financial enterprise complies with regulatory standards and that its risk management processes are successful, while managers are utilizing technology in audit management software to streamline all these processes.

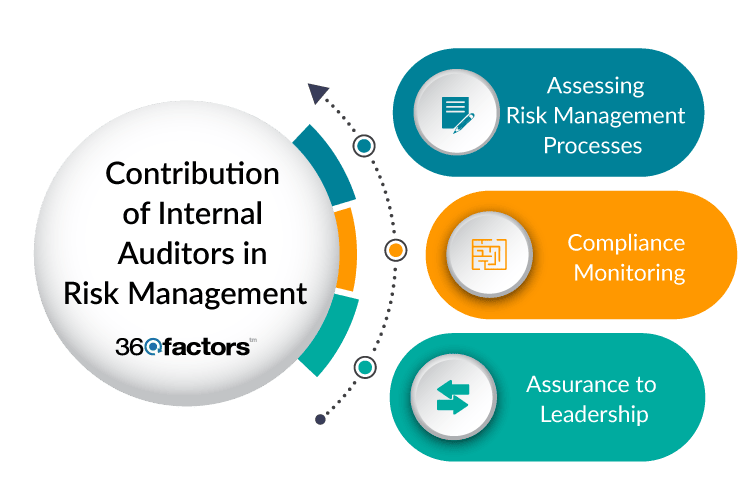

Contribution of Internal Auditors in Risk Management

In the broader ecosystem of organizational governance, internal auditors are significant contributors rather than gatekeepers to successful risk management. Their crucial role in internal audit and risk management goes beyond conventional auditing and extends to risk detection, evaluation, and reduction.

As organizations deal with an ever-evolving environment of challenges and risks, the contributions of internal auditors become progressively undeniable. Let’s dive into the three main contributions of internal auditors and risk management personnel:

Role in Assessing Risk Management Processes

Internal auditors are responsible for regularly evaluating an organization’s risk management program, specifically regulatory risks. The report generated by the internal auditors is the foundation for consistent enhancement, highlighting gaps and enabling risk monitoring teams to execute robust control measures for effective internal audit and risk management.

Compliance Monitoring

Compliance monitoring, a key function of auditors, provides companies with the guarantee that they are successfully meeting the requirements set by regulators. It is imperative to understand the different roles that compliance and internal audit teams play here for success. While the former focuses on ongoing policy and process assessment, the latter offers a snapshot of compliance at a particular period of time.

Assurance to Leadership

The primary goal of the internal audit management function is to assure the board and senior leadership of the organization’s risk management effectiveness. This assurance serves two purposes.

First, it ensures that substantial business risks are managed successfully. Second, it guarantees that various procedures are being supervised efficiently. In this way, the business leadership can be confident about the effectiveness of internal audit and risk management procedures.

Difference Between Internal Auditing and Risk Management Roles

Both risk management and internal audit are essential components of an organization’s governance structure. While they contribute to the common goals of ensuring organizational integrity and compliance, their roles and accountabilities are distinct. Getting to know these differences is vital for successful governance.

Let’s explore the main differences between the internal audit and risk management functions in an organization:

Risk Management

Framework Development: Risk management creates a robust risk management framework. This framework sets the parameters for identifying, assessing, and managing potential threats.

Framework Implementation: Risk management guarantees successful implementation of risk management framework throughout the organization and goes beyond just developing the framework.

Operational Integration: Risk management offers guidance on integrating risk consequences into daily business operations, guaranteeing that risk awareness is part of the organizational culture.

Accountability Allocation: Risk management’s role is to provide guidance on who should be responsible for explicit risks, controls, and tasks. It ensures the design of all strategies while keeping the audit scheduling in mind so that all risk management steps can go smoothly.

Internal Audit

Framework Evaluation: Internal audit measures the competence and effectiveness of the risk management framework, ensuring it’s not just a paper exercise. This is one of the main differences between internal audit and risk management.

Implementation Checks: Internal audit evaluates the actual implementation of the risk management framework, guaranteeing that it’s practiced as intended. In this way, it functions as a check on the risk management framework.

Management Commitment Review: One of the critical tasks of internal audit is to evaluate the commitment level of management towards risk management.

Objective Assurance: Internal audit offers unbiased findings on the risk management information presented to the board, ensuring its precision and relevance. There is a point to be noted here. There is a convergence of interests between internal audit and risk management. For instance, both might analyze and interpret risk management data for the board. Hence, if the coordination between these two functions is poorly managed, such overlaps can lead to potential conflicts of interest.

Why Bring Them Together?

The primary role of risk managers is to lead ERM within the company, whereas the internal auditor’s role is to evaluate the ERM process the risk manager supervises. The users or decision-makers need reliable and authentic data to drive strategy.

The internal auditor’s assurance regarding ERM for evaluating risk reporting and management procedures leads to enhanced confidence in the reports. There is a need for a synergetic association between risk managers and internal auditors. Cooperation for the design of internal audit management assurance plans ensures internal audit and risk management approach.

Streamline Internal Audit Processes to Mitigate Risk with Technology

The traditional internal auditing methods, which relied heavily on manual processes, are becoming increasingly obsolete. These methods are time-consuming, prone to errors, and must be more agile in today’s fast-paced business environment. Enter technology. With the advent of advanced software solutions, such as Predict360’s Internal Audit and Findings Management Software, you can enjoy significant benefits:

Automated Workflows: Gone are the days of manual data entry and tedious paperwork. Predict360 Internal Audit and Findings Management Software automates routine tasks, allowing auditors to focus on areas that require critical analysis. This feature helps managers focus more on internal audit and risk management gaps.

Real-time Reporting: Instant access to audit reports, dashboards, and critical metrics ensures that stakeholders are always informed and can make timely decisions.

Audit Plans Notifications: Create audit plans, checklists and notifications for designated audit dates to safeguard timely audits.

Integrated Risk Frameworks: The internal audit software module can integrate with Predict360 Risk and Compliance modules for augmented audit management, risk assessments, and analytics.

Request a Demo

Complete the form below and our business team will be in touch to schedule a product demo.

By clicking ‘SUBMIT’ you agree to our Privacy Policy.

Stay Informed About Upcoming Webinars & Events!