Home/ Blog / How AI in the Insurance Industry is Influencing Regulatory Changes in 2024

As we enter 2024, the adoption of AI in the insurance industry is not just a buzzword but a transformative force reshaping the sector. Integrating AI technologies in insurance operations revolutionizes various services, from risk assessment to customer engagement. However, this evolution also brings a wave of regulatory change, challenging insurers to navigate a landscape where innovation must meet compliance.

The insurance industry is witnessing a significant shift towards AI and machine learning (ML) applications in the United States. This trend demonstrates technological advancement and responds to the growing demands for efficiency, accuracy, and personalized services in the insurance sector. As business leaders’ interest in AI in the insurance industry continues to grow, it becomes crucial to understand the implications of this integration in terms of operational enhancements and the context of regulatory compliance and ethical considerations.

In the following blog sections, we will explore the rise of AI in insurance sector, the regulatory response to these advancements, and the strategies that firms should adopt to manage regulatory change and compliance challenges effectively in this dynamic landscape.

The Rise of AI in Insurance

The regulatory landscape is shifting rapidly due to AI technological advancements, with regulatory change becoming a pivotal aspect of this transformation. Regulatory bodies are now more focused than ever on ensuring that the deployment of AI in the insurance industry aligns with legal and ethical standards, safeguarding consumer interests while promoting innovation. This balance between technological growth and regulatory change management compliance is vital for the industry’s sustainable development.

The integration of AI is not just a trend in the insurance industry; it’s a transformative force reshaping the sector. According to a National Association of Insurance Commissioners (NAIC) survey, an impressive 70% of homeowners’ insurance companies and a staggering 88% of private passenger insurers are either planning to use, currently using, or exploring the use of AI and machine learning (ML) in their operations. This significant adoption of AI in the insurance industry indicates the technology’s growing influence.

AI’s application is most prominent in claims processing, including subrogation claims triage and evaluating images of accidental losses. Its use closely follows this in underwriting, marketing, fraud detection, rating, and loss prevention. The impact of AI on these areas is profound, offering enhanced efficiency and accuracy, which are crucial in the fast-paced insurance environment.

Regulatory Response to AI Advancements

As the popularity of AI in the insurance industry grows, regulatory bodies actively respond to technological advancements. Integrating AI in insurance operations, from claims processing to fraud detection, has necessitated a significant regulatory change and compliance management shift. There are various types of risks affecting the insurance sector, and there must be effective tactics to deal with them. The National Association of Insurance Commissioners (NAIC) has been at the forefront of this shift, particularly with the development of the AI Model Bulletin.

The AI Model Bulletin, adopted in December 2023, represents a landmark regulatory policy for AI in the insurance industry. The industry has endorsed this principles-based approach despite some concerns from consumer advocates. The bulletin does not create new laws but serves as crucial guidance. It emphasizes that decisions impacting consumers, made or supported by AI systems, must comply with all applicable insurance laws and regulations, including those governing unfair trade practices.

Key principles of the NAIC’s AI Model Bulletin

Compliance with Insurance Laws: AI systems must adhere to all applicable insurance laws, ensuring fair and ethical treatment of consumers.

Transparency: There is an emphasis on ethics when adopting AI in the insurance industry, with focus on the transparency of AI decisions and outcomes, and making them understandable to the impacted consumers.

Human Oversight: The bulletin advocates for human involvement in AI decision-making processes, ensuring that technology complements rather than replaces human judgment.

Third-Party Data and Model Usage: Insurers using third-party services, data and models must ensure these external resources comply with the same standards expected of the insurers.

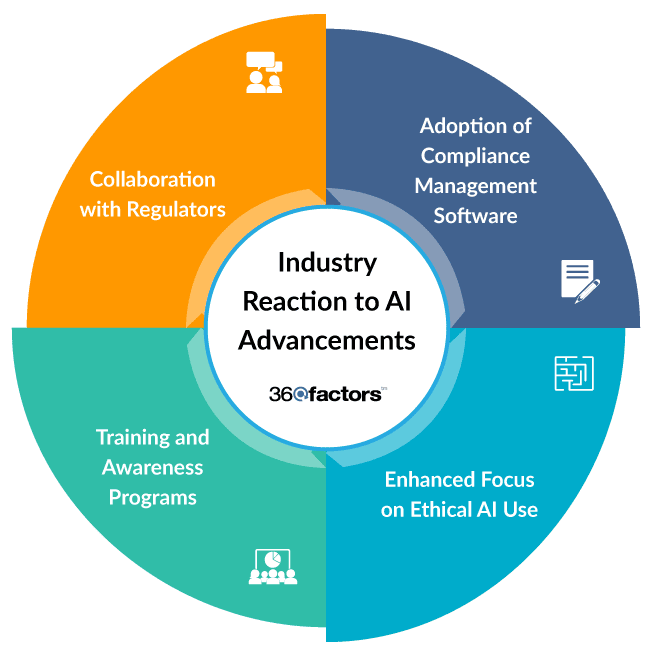

Industry Reaction

The insurance industry’s reaction to these regulatory changes has been multifaceted. Companies are adapting their strategies to align with the new regulatory landscape, focusing on regulatory compliance management software and systems to ensure adherence to these guidelines.

Adoption of Compliance Management Software: Many insurers are turning to regulatory compliance software to manage the complexities of adhering to the new guidelines surrounding AI in the insurance industry.

Enhanced Focus on Ethical AI Use: There is an increased emphasis on developing AI systems that are unbiased and fair, with insurers investing in technologies and practices that promote ethical AI.

Collaboration with Regulators: Insurers are engaging more with regulatory bodies to understand and influence the evolving landscape of AI regulation.

Training and Awareness Programs: Companies are implementing training programs to educate their staff about the importance of regulatory compliance and ethical AI use.

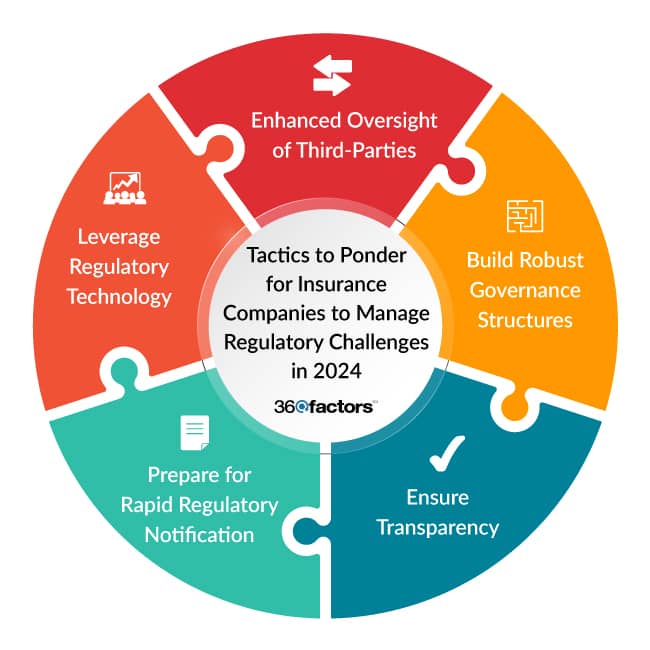

Tactics to Consider for Insurance Companies to Manage Regulatory Challenges in 2024

As AI in the insurance industry evolves, insurance companies face the daunting task of keeping up with regulatory changes and ensuring compliance. In 2024, a key tactic for these companies is to leverage advanced regulatory change management strategies. Some other tactics are outlined below:

1. Enhanced Oversight of Third-Party Providers

Insurers need to oversee third-party data providers rigorously. This includes ensuring their AI systems and models comply with state laws and regulations.

2. Building Robust Governance Structures

Insurance companies should build governance structures that incorporate policy, standards, defined roles for personnel, monitoring, and testing, especially in order to implement AI in the insurance industry. This includes conducting impact/risk assessments and integrating third-party privacy programs.

3. Ensuring Transparency

Insurers must strive for their models’ processes to be explainable for all data use. This means making it clear to consumers and regulators how their models, including third-party ones, are built and work and how they are performing.

4. Preparation for Rapid Regulatory Notification

Insurers should have systems in place to notify regulators promptly of cyberattacks and ransom payments, as required by regulations like those in New York.

5. Leverage Regulatory Technology

Adopting an effective regulatory technology platform that integrates AI in the insurance industry helps manage multiple challenges.

One of the best RegTech platforms is Predict360 Regulatory Change Management Software; it enhances RCM with Regulatory Change Tracking, Activity Management, and Artificial Intelligence (AI). Key Features of Predict360 that make it beneficial for the Insurance Industry include the following:

Regulatory Intelligence and Updates

Predict360 RCM tool consolidates regulatory intelligence, updates, and news from various external sources into one feed, ensuring that insurance companies are always up-to-date with the latest regulatory changes.

Automated Impact Assessment

The RCM software offers an automated preliminary assessment of the impact of changes, identifying the business units affected based on risk mapping. This feature is crucial for insurance companies to understand how new regulations might affect their operations, especially in the context of the growing integration of AI in the insurance industry.

Integrated Regulatory Intelligence Feeds

Predict360 RCM application integrates regulatory intelligence feeds with project plans that track and manage multiple tasks. This integration is vital for managing regulatory examinations and findings effectively.

Automated Notifications

The Predict360 RCM platform sends automated notifications to relevant stakeholders about all related audits, policies, rules, and documents affected by changes. This ensures that all departments within an insurance company are aligned and informed about regulatory policy changes.

Real-Time Executive View

Predict360 RCM Software provides a real-time executive view of regulatory issues across the organization, enabling decision-makers to comprehensively understand the regulatory landscape and its impact on their business.

Conclusion

As we wrap up our exploration of AI in the insurance industry and its impact on regulatory change in 2024 impact on regulatory change in 2024, it’s clear that the landscape is rapidly evolving. Integrating AI technologies in insurance processes, from claims handling to fraud detection, is transforming the industry and reshaping the regulatory framework.

The dynamic nature of AI technology and the regulatory landscape demands agility and foresight from insurance companies. Staying informed about regulatory developments and being ready to adapt quickly is crucial to managing these changes effectively. Embracing the potential of AI in the insurance industry while being mindful of its challenges will be critical in navigating the future.

By adopting a proactive approach, including implementing Predict360 Regulatory Change Management Software, insurance companies can track regulatory requirements, changes, updates, news, and notifications and then manage all activities and documents related to those regulatory updates at enterprise level.

Request a Demo

Complete the form below and our business team will be in touch to schedule a product demo.

By clicking ‘SUBMIT’ you agree to our Privacy Policy.

Stay Informed About Upcoming Webinars & Events!